Thailand’s pharmaceutical industry is one of the most strategically significant in Southeast Asia — a third-place market by size, a government-designated Medical Hub priority sector, and an increasingly active destination for both generic drug manufacturing investment and emerging biologics production ambitions. For pharma companies, medical nutrition businesses, and biotech investors assessing ASEAN, Thailand offers a combination of established market infrastructure, universal health coverage-driven demand, and a regulatory and incentive environment that has grown meaningfully more investor-friendly in recent years.

Table of Contents

- Market Size and Growth

- Key Market Segments: Original and Generic Drugs

- Major Pharmaceutical Companies in Thailand

- Government Initiatives and BOI Incentives 2026

- Biologics, Biosimilars, and Biotech in Thailand

- AI in Pharmaceutical Development

- Regulatory Framework: Thai FDA

- Challenges in Thailand’s Pharma Market

- Healthcare Market Research in Thailand

- Sources

Market Size and Growth

Thailand’s pharmaceutical market reached approximately 240 billion baht in 2024, up from 212 billion baht in 2023, making it the third-largest pharma market in Southeast Asia. According to Krungsri Research’s Industry Outlook 2025–2027, domestic drug sales are projected to grow 6.0–7.0% annually through 2027, driven by the aging population, rising NCD prevalence, and government healthcare spending commitments. Grand View Research projects the market will reach USD 13.9 billion (approximately 480 billion baht) by 2030, implying a CAGR of 7.7%.

Three structural demand drivers underpin this growth trajectory. First, Thailand’s demographic shift: people aged 60 and above now exceed 21% of the population, creating sustained, predictable demand for chronic disease medications across cardiovascular, diabetes, and oncology categories. Second, the Universal Coverage Scheme (UCS), which the government expanded significantly in 2025 with a budget allocation of THB 235 billion — an 8.3% increase — broadening access to treatments including cancer care and type-2 diabetes management. Third, the country’s thriving medical tourism sector, which brings approximately 2 million international patients annually into Thailand’s private hospital system, generating additional pharmaceutical demand outside the domestic insurance framework.

Pharmaceuticals account for 29% of all national healthcare spending in Thailand, with 90% of domestic production consumed domestically and the remaining 10% exported primarily to Vietnam, Myanmar, and Cambodia.

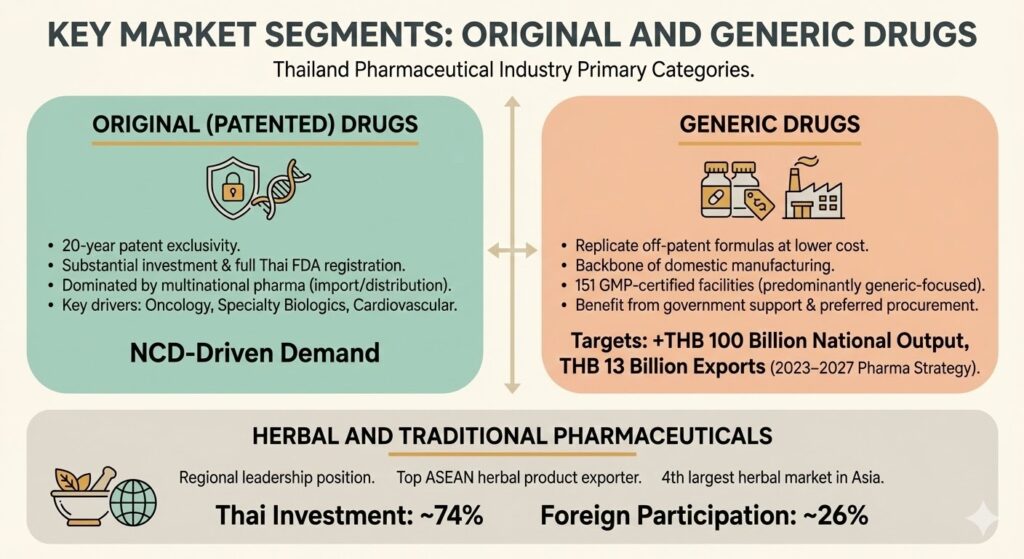

Key Market Segments: Original and Generic Drugs

The pharmaceutical industry in Thailand operates across two primary categories.

Original (patented) drugs require substantial investment in development, carry 20-year patent exclusivity, and must complete full registration with the Thai FDA prior to market launch. Multinational pharma companies in Thailand dominate this segment, primarily through import and distribution rather than local manufacturing. The segment is driven by oncology, specialty biologics, and cardiovascular therapies — areas with growing NCD-driven demand and expanding UCS coverage.

Generic drugs are the backbone of Thailand’s domestic pharmaceutical manufacturing. Local producers replicate off-patent formulas at significantly lower cost, serving both the public health system and the domestic retail market. Thailand’s 151 GMP-certified manufacturing facilities are predominantly generic-focused. Generic drugs benefit from the government’s active support for domestic production security — the 2023–2027 pharma strategy targets an increase of THB 100 billion in national pharmaceutical output and growth in export markets to THB 13 billion. Generic drug manufacturers also benefit from preferred procurement status under the public health insurance schemes.

Herbal and traditional pharmaceuticals represent a further segment where Thailand has genuine regional leadership. The country is the top herbal product exporter in ASEAN and holds the fourth-largest herbal market position in Asia. Thai investors account for approximately 74% of total herbal sector investment, with foreign participation making up the remaining 26%.

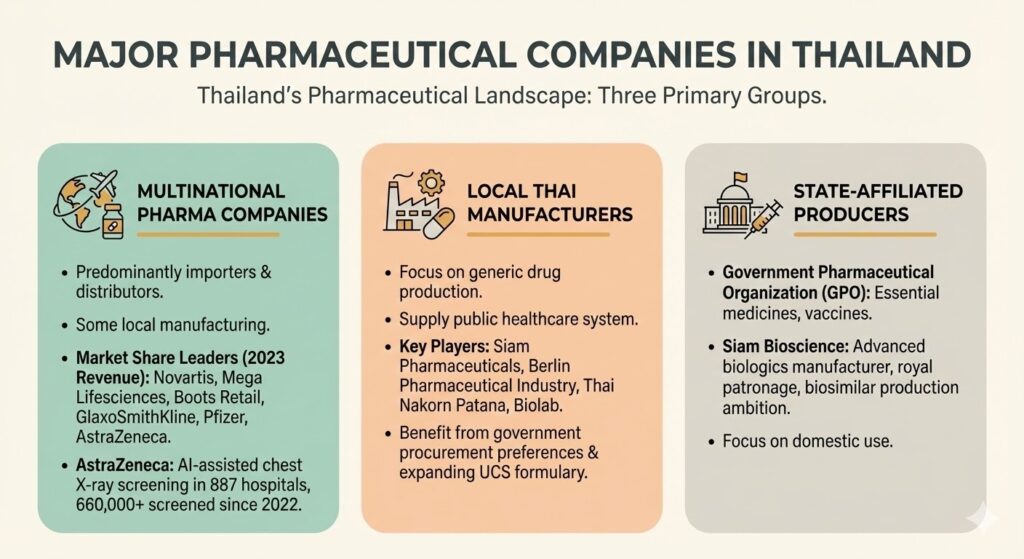

Major Pharmaceutical Companies in Thailand

Thailand’s pharmaceutical landscape divides into three groups.

Multinational pharma companies operate predominantly as importers and distributors, with some maintaining local manufacturing for specific product lines. Based on Krungsri Research data, Novartis held the largest market share among private pharmaceutical companies in Thailand by revenue in 2023, followed by Mega Lifesciences, Boots Retail, GlaxoSmithKline, Pfizer, and AstraZeneca. AstraZeneca has a particularly active local footprint beyond distribution — its AI-assisted chest X-ray screening program has been deployed across 887 hospitals through a partnership with the National Health Security Office, screening over 660,000 people in Thailand since 2022.

Local Thai manufacturers focus primarily on generic drug production and supply to the public healthcare system. Key players include Siam Pharmaceuticals, Berlin Pharmaceutical Industry, Thai Nakorn Patana, and Biolab. These companies benefit from government procurement preferences and the expanding UCS drug formulary.

State-affiliated producers include the Government Pharmaceutical Organization (GPO), which manufactures essential medicines, vaccines, and — through Siam Bioscience — biologics for domestic use. Siam Bioscience, backed by royal patronage, is Thailand’s most advanced biologics manufacturer and the most visible example of the country’s ambitions in biosimilar production.

Government Initiatives and BOI Incentives 2026

Thailand’s government has made pharmaceutical manufacturing a priority investment sector under both the Medical Hub 2025–2034 strategy and the Thailand 4.0 New S-Curve industrial framework. For pharma investors, the practical entry point is the BOI incentive structure.

BOI incentives for pharmaceutical manufacturing are structured under the A1 and A2 categories for most pharmaceutical activities, with biotechnology development qualifying for the most generous A1+ tier — up to 10 years of corporate income tax exemption with no cap on the amount. Specific qualifying activities include:

- Manufacture of pharmaceutical products (A2 category: up to 8 years CIT exemption)

- Manufacture of biological substances using microorganisms, plant cells, and animal cells (A1)

- Manufacture of bio-molecules and bioactive substances (A1)

- Biotechnology development with technology transfer to an approved educational or research institution (A1+: 10 years, no CIT cap)

All BOI-promoted pharma projects qualify for non-tax incentives including the right to own land, the right to bring in foreign skilled workers and experts, and import duty exemptions on machinery and raw materials.

For companies assessing whether their specific product or manufacturing activity qualifies under BOI categories, and what the realistic approval timeline looks like, a feasibility study is the appropriate first step before capital commitment.

Biologics, Biosimilars, and Biotech in Thailand

Biologics manufacturing is the most significant content gap in most analyses of Thailand’s pharma sector — and the single most commercially consequential development for multinational pharma and biotech investors assessing the country.

Thailand has had formal biosimilar guidelines since 2013, aligned with WHO standards and ASEAN harmonisation frameworks. The Thai FDA’s approach requires the same preclinical and clinical comparability data that the US FDA and EMA demand — a standard that puts Thailand’s regulatory pathway for biosimilars on credible international footing. This matters for manufacturers because it means biosimilars approved in Thailand carry regulatory credibility for export into other ASEAN markets that reference Thai approvals.

Biotech more broadly is an active investment category in Thailand. The National Science and Technology Development Agency (NSTDA) and the Thailand Center of Excellence for Life Sciences provide public-private partnership frameworks for biotech R&D investment.

AI in Pharmaceutical Development

AI in pharmaceutical development is reshaping the industry’s cost and timeline economics globally, and Thailand is not insulated from this shift — nor is it standing still.

At the global level, AI is demonstrably compressing early-stage drug discovery timelines. Traditional preclinical candidate development takes three to four years; AI-assisted approaches are achieving this in 13 to 18 months in documented cases. AI can accelerate early-stage discovery timelines by an estimated 30–40%, though the fundamental challenge of clinical success rates — which remain stubbornly around 10% for candidates entering Phase I — has not yet been resolved by AI. The US FDA’s January 2025 draft guidance on AI use in regulatory decision-making signals that this technology is transitioning from experimental to expected in serious pharmaceutical development programmes.

Regulatory Framework: Thai FDA

The Food and Drug Administration of Thailand, operating under the Ministry of Public Health, governs the registration and post-market surveillance of pharmaceuticals, biologics, and medical devices through the Drug Act B.E. 2510 (1967) and the Medical Device Act B.E. 2551 (2008).

For finished pharmaceutical products intended for general sale, manufacturers and importers must first obtain a drug facility licence before proceeding to product registration. Registration documentation follows either the ASEAN Common Technical Dossier (ACTD) or the ICH Common Technical Document (ICH CTD) format. The Thai FDA’s requirements for biologics registration are aligned with WHO standards, and biosimilar approval requires the comparability data — preclinical and clinical — that international regulators expect.

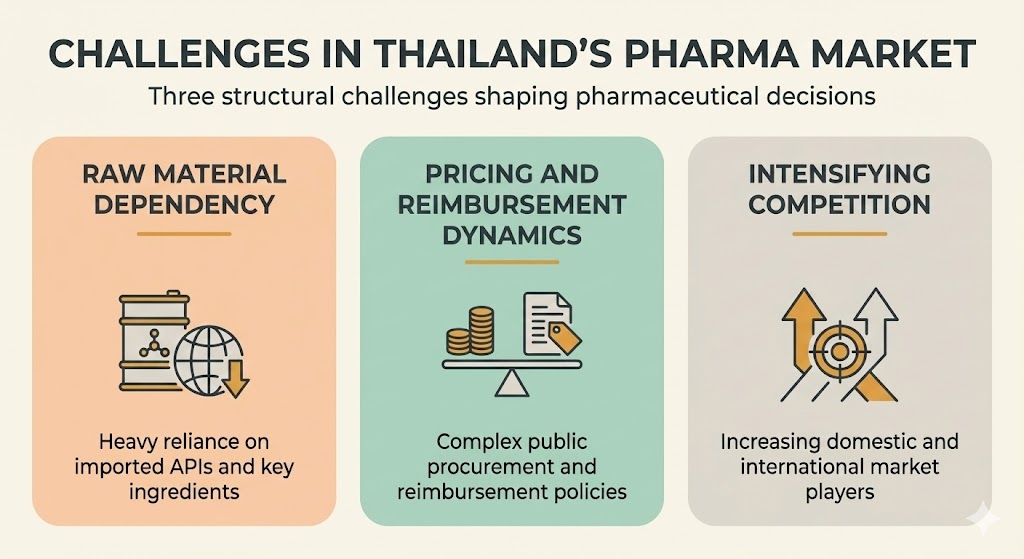

Challenges in Thailand’s Pharma Market

Three structural challenges shape the decisions of pharmaceutical companies operating in or entering Thailand’s market.

Raw material dependency. Thailand’s pharmaceutical manufacturing base imports the majority of its active pharmaceutical ingredients, primarily from India and China. This dependency creates margin pressure and supply security risk — concerns that have intensified since the pandemic-era supply chain disruptions. The government’s 2023–2027 domestic production strategy explicitly targets reducing API import dependency, but change is gradual. For MNCs, this shapes how local manufacturing economics are modelled.

Pricing and reimbursement dynamics. Thailand operates three major public health insurance schemes — the Universal Coverage Scheme, Civil Servant Medical Benefit Scheme, and Social Security Scheme — each with distinct formularies, procurement mechanisms, and pricing dynamics. Public hospital procurement dominates drug sales by value, with hospitals accounting for 80% of total drug sales and public hospitals alone representing 60%. Pricing negotiations with the NHSO and public procurement bodies require a different strategy than private market sales, and the dynamics are not immediately transparent to companies entering from markets with different reimbursement structures.

Intensifying competition. The past five years have seen significantly increased foreign investment in Thailand’s generic manufacturing base — particularly from Chinese and South Korean players. Over 2020–2023, Chinese pharmaceutical companies submitted 23 BOI applications for medical industry investment worth THB 3.09 billion, up from just 3 projects in 2018–2019. South Korean companies submitted projects valued at THB 10.02 billion over the same period. This competitive dynamic is reshaping margin expectations for generic drug manufacturers and accelerating the pressure on Thai incumbents to move up the value chain.

Healthcare Market Research in Thailand

At Iconic Research, we conduct pharmaceutical market research across Rx, OTC, biologics, and medical nutrition categories.

Two examples of our work:

Blood Disorders — Pharmaceutical Market Entry

Medical Nutrition — Patient and HCP Research

For pharma companies assessing market entry, our market entry insights provide the strategic intelligence needed before committing to Thailand. For companies already operating in the market and tracking competitive positioning, see our market research services in Thailand. For companies validating new pharmaceutical concepts or formulations before investment, our concept testing and pre-validation services are designed for this stage.

Frequently Asked Questions

How large is Thailand's pharmaceutical market in 2026?

Approximately 240 billion baht as of 2024, growing at 6–7% annually through 2027 per Krungsri Research, making it Southeast Asia's third-largest pharma market.

Which are the leading pharma companies in Thailand?

By revenue, Novartis leads among private sector companies, followed by Mega Lifesciences, GlaxoSmithKline, Pfizer, and AstraZeneca. The state-affiliated Government Pharmaceutical Organization (GPO) and Siam Bioscience are significant domestic producers.

What BOI incentives are available for pharmaceutical investment in Thailand?

Up to 8 years of CIT exemption for standard pharmaceutical manufacturing, up to 10 years with no cap for biotechnology development with technology transfer, plus import duty waivers on machinery and the right to own land.

Is Thailand developing a biologics and biosimilars manufacturing industry?

Yes. Thailand has had formal biosimilar guidelines since 2013 aligned with WHO standards. Siam Bioscience is the country's most advanced biologics manufacturer, and the BOI's A1+ category specifically incentivises biologics and biotechnology investment with the maximum available tax exemption.

How does Thailand's regulatory pathway work for pharmaceutical registration?

Products must be registered with the Thai FDA following ACTD or ICH CTD guidelines, with a mandatory facility licence required first. Biologics and biosimilars require full comparability data per WHO standards. Timelines and practical navigation differ from published guidelines — a feasibility study is recommended before committing.

Sources

- Krungsri Research. Industry Outlook 2025–2027: Pharmaceuticals. https://www.krungsri.com/en/research/industry/industry-outlook/chemicals/phamaceuticals/io/io-pharmaceuticals-2025-2027

- Grand View Research / Horizon Databook. Thailand Pharmaceutical Market Size & Outlook 2025–2030. https://www.grandviewresearch.com/horizon/outlook/pharmaceutical-market/thailand

- Board of Investment Thailand. Investment Promotion Guide 2025. https://osos.boi.go.th/download/BOI_PDF/BOI_A_Guide2025_EN.pdf

- ASEAN Journal of Radiology. Thailand is Implementing Artificial Intelligence to Assist Interpreting Chest Radiographs in Public Health. https://asean-journal-radiology.org/index.php/ajr/article/view/988

- Biosimilar Development. The Thai FDA’s Approach to Biologics and Biosimilars. https://www.biosimilardevelopment.com/doc/the-thai-fda-s-approach-to-biologics-and-biosimilars-0001

If you wish to quote any information from this article, please kindly cite the source along with the link to the original article to respect copyright. |

Iconic Research Thailand Your trusted partner in market research and consulting across Thailand and Southeast Asia. Headquartered in Bangkok, we provide research-driven insights across the Philippines, Malaysia, Indonesia, Singapore, Laos, and Vietnam. We help businesses navigate Thailand's market complexities through consumer insights, market entry strategy, and trend foresight. Contact us if you have any queries! (+66)888 954 954 |

Contact us

We always looking for new and exciting opportunities. Let’s connect.

Related posts

AI Thailand: The Opportunity Is Real, But So Is the Complexity

AI Thailand: The Opportunity Is Real, But So Is the Complexity

Thailand’s AI market is projected to reach 114 billion baht by 2030, yet most Thai consumers remain cautious. Understanding who they are – and what they actually need from AI – is the difference between a product that lands and one that doesn’t.

13 min read Thailand 4.0 in 2026: An Investor’s Blueprint for the Innovation Economy

Thailand 4.0 in 2026: An Investor’s Blueprint for the Innovation Economy

Thailand 4.0 has reached a defining year in 2026 – transitioning from policy vision to operational reality with AI integration, EV manufacturing, and digital infrastructure driving the innovation economy.

9 min read Unlocking the “Why” Behind Thai Culture: Introducing PhumPanya

Unlocking the “Why” Behind Thai Culture: Introducing PhumPanya

Thai culture can feel like a puzzle. At PhumPanya, we believe the key to understanding Thai language and culture is in the words themselves. Explore our free database of Thai words, their roots, and the cultural logic hidden inside the language.

3 min read