FinTech in Thailand refers to the ecosystem of financial technology companies, digital banking platforms, payment infrastructure, and regulatory frameworks operating within Thailand’s financial services market. It encompasses digital wallets, virtual banks, real-time payment systems like PromptPay, and API-driven banking services — supported by the Bank of Thailand through sandbox programmes, virtual bank licensing, and open banking standards. With 177 fintech companies, 92% digital payment adoption, and over 75 million daily PromptPay transactions, Thailand ranks among Southeast Asia’s most advanced fintech markets. Leaders like SCB 10X and Krungsri are deploying AI for personalisation and blockchain for cross-border payments, while newly licensed virtual banks intensify competition.

Table of Contents

- What is FinTech?

- FinTech Thailand: Sector Overview and Key Metrics

- Digital Banking in Thailand

- The Wallet Wars: Thailand’s E-Payment Ecosystem

- Case Study: Digital Banking User Experience Research

- PromptPay and Open Banking Infrastructure

- The Future of FinTech and Digital Banking in Thailand

- Conclusion & TL;DR

- References

What is FinTech?

FinTech — short for financial technology — refers to digital solutions that disrupt or enhance traditional financial services through automation, accessibility, and user-centric design. In Thailand, fintech reflects both local consumer needs and regulatory frameworks that promote innovation while ensuring financial stability.

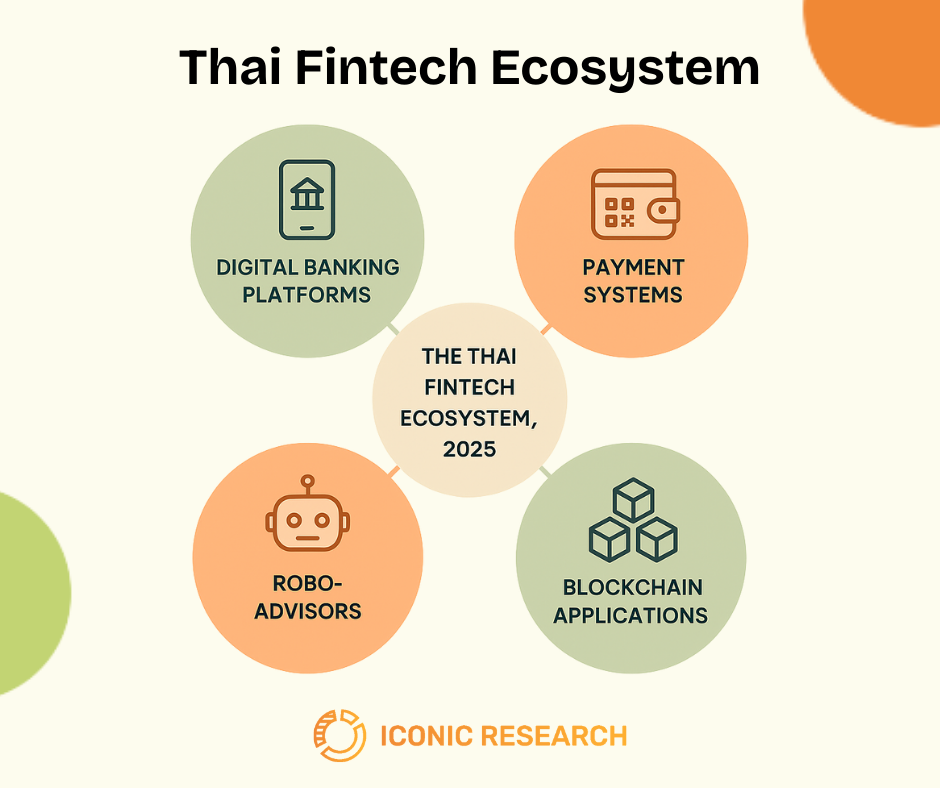

The Thai fintech ecosystem encompasses digital banking platforms, payment systems, blockchain applications, and robo-advisors. What makes Thailand unique is how quickly traditional financial institutions have embraced collaboration rather than competition with fintech innovators, creating an integrated landscape serving both urban professionals and rural communities.

FinTech Thailand: Sector Overview and Key Metrics

Fintech Thailand has become one of Southeast Asia’s most dynamic hubs, home to 177 fintech companies growing at 12.8% annually [4]. Payments remain the largest segment among fintech companies, but growth is accelerating in blockchain, insurtech, and regtech. On the consumer side, digital adoption is widespread: 92% of Thais use digital payments, and PromptPay processes over 75 million daily transactions. Mobile-first behaviour, QR code ubiquity, and the rise of digital wallets such as TrueMoney and Rubie Wallet are transforming how money moves across the economy.

Traditional banks remain dominant in asset share but are rapidly digitising through comprehensive bank digital transformation strategy initiatives. Institutions like Krungsri and SCB are investing in AI-driven personalisation, blockchain-based payments, and API-first platforms while modernising digital channels. At the same time, newly licensed virtual banks are entering the market, targeting underserved populations and intensifying competition. With strong regulatory backing from the Bank of Thailand (BOT) — through sandbox programmes, ISO 20022 adoption, and virtual bank licensing — Thailand’s fintech ecosystem is evolving into an interoperable financial infrastructure that blends traditional banking trust with fintech agility.

Digital Banking in Thailand

Digital banking in Thailand is shifting from pilot projects to large-scale transformation. As consumer demand grows and fintech competition intensifies, banks are reengineering legacy systems into cloud infrastructure platforms and API-first architectures. The Bank of Thailand (BOT) has introduced new digital bank licences under its framework — a move that is reshaping the country’s financial landscape.

Rise of Virtual Banks (New Licences)

The BOT has issued three virtual bank licences, with operations expected by 2026. These fully digital institutions will operate without physical branches, offering AI-driven credit scoring, seamless onboarding, and embedded finance to underserved customers, boosting financial inclusion for retail and SME segments that traditional banking channels have struggled to reach [3].

Case Studies: SCB, Krungsri, Kasikornbank

Incumbent banks are implementing sophisticated bank digital transformation strategy approaches through tech-focused subsidiaries:

- SCB TechX develops scalable digital banking platforms and AI-powered services to position SCB as a regional fintech leader

- KBTG (Kasikornbank) emphasises open APIs and ecosystem integration to unlock new revenue streams through wealth management and embedded finance

- Krungsri Finnovate invests heavily in blockchain and AI technologies to streamline cross-border payments

Challenges: Regulation, Trust, Debt

Despite strong momentum, significant hurdles remain: evolving rules for digital assets and consumer protection create compliance uncertainty, many consumers outside urban centres remain cautious about fully digital banking, and Thailand’s persistently high household debt levels require responsible fintech-driven lending practices.

The Wallet Wars: Thailand’s E-Payment Ecosystem

Payments have always been the beating heart of fintech in Thailand, and competition is fiercest in the digital wallet space. For many Thais, wallets like TrueMoney, ShopeePay, Rabbit LINE Pay, and SCB Easy are the most visible face of fintech — used daily for shopping, transport, remittances, and bills. This wallet competition reflects how fintech is reshaping the thai banking industry, embedding financial services into e-commerce, social platforms, and everyday routines.

Leading players [1] dominate the market:

- TrueMoney holds the largest user base with broad merchant acceptance and leadership in cross-border remittances

- ShopeePay integrates seamlessly with Shopee e-commerce, driving adoption among online shoppers

- Rabbit LINE Pay leverages LINE’s messaging platform to embed payments into lifestyle interactions

- SCB Easy offers traditional bank trust with digital convenience

E-Payment Player | Key Strengths | Competitive Strategy | User Focus / Positioning |

TrueMoney | Largest user base, early market entry, wide merchant acceptance | Loyalty programs, rewards, exclusive merchant partnerships | Broad user base, widespread everyday payments |

ShopeePay | High transaction volume, seamless integration with Shopee e-commerce | Drive convenience for online shoppers via platform synergy | E-commerce shoppers, digital convenience |

Rabbit LINE Pay | Social & lifestyle integration via LINE messaging platform | Embedding payments into daily social interactions | Social users, lifestyle-oriented consumers |

SCB Easy | Bank-owned wallet, trusted brand, blends banking & digital convenience | Combines legacy finance trust with modern digital features | Traditional banking users adapting to digital wallets |

Understanding these market dynamics requires comprehensive market research to uncover user preferences, adoption drivers, and competitive positioning. With multiple players competing for wallet share, financial institutions need deep consumer insights to identify which features resonate most with different demographic segments, how users actually interact with these platforms, and what factors influence switching behaviour between wallets.

Market Growth & Competition Models

Thailand’s digital wallet market expanded at 18.1% CAGR between 2020 and 2024 and is forecast to surpass USD 30 billion by 2029. Wallets now handle 23% of e-commerce transactions.

Competition follows two models: bank-owned wallets like SCB Easy build on consumer trust and regulatory compliance, expanding into lending and deposits. Platform-native wallets such as TrueMoney and ShopeePay focus on convenience, lifestyle services, and ecosystem integration, gaining traction through e-commerce and social networks.

By embedding payments into daily routines — transportation, food delivery, and entertainment — digital wallet platforms enhance user engagement and transaction frequency. Additionally, many are leveraging transaction data to offer lending and credit services, using built-in risk assessments to deliver seamless financial products. This backend integration deepens customer relationships and moves wallets beyond payment tools into full-service financial platforms.

Aspect | Bank-Owned Wallets (e.g., SCB Easy) | Platform-Native Wallets (e.g., TrueMoney, ShopeePay, Rabbit LINE Pay) |

Strengths | Trusted brand, integrated with banking services, regulatory compliance | Large user base from platform ecosystems, strong lifestyle engagement |

Focus | Financial services expansion, lending, deposits | Payment convenience, merchant partnerships, lifestyle services |

User Acquisition | Leverages existing bank customers | Leverages platform users and social networks |

Innovation | API integration, product modernization | Rapid feature rollout, ecosystem expansion |

Case Study: Digital Banking User Experience Research

We helped one of Thailand’s major banks improve their struggling mobile banking app through comprehensive user feedback analysis. Using in-depth interviews with diverse customer segments, we identified critical usability issues that were driving poor app store ratings and increased support calls, providing actionable insights that transformed their digital banking experience.

This work reflects a broader pattern in Thailand’s financial services market. A digital banking platform that tests well in Singapore or Korea will not automatically land with Thai consumers — the usage patterns, trust signals, and switching behaviour are different. Understanding those differences through consumer insights research and UX research is what separates a successful product launch from a costly correction.

PromptPay and Open Banking Infrastructure

Thailand’s digital payment ecosystem is anchored by PromptPay, with more than 77 million registrations and nearly 76 million daily transactions [2]. PromptPay has become the backbone of open banking infrastructure, enabling instant, low-cost transfers that support financial inclusion and demonstrate how technology is reshaping traditional banking through seamless interoperability.

Interoperability & Cross-Border Integration

PromptPay operates through the National ITMX switch, connecting over 30 banks and financial institutions. Standardised QR codes, used monthly by over 60% of Thais, integrate with global networks like Visa, Mastercard, and UnionPay [2]. ISO 20022 messaging standards and open APIs enable real-time interoperability across the Thai banking industry.

Cross-border linkages connect PromptPay to Laos, Cambodia, Malaysia, and Singapore, with expansion to Japan and China underway. These initiatives enable local currency payments without US dollar intermediaries, transforming financial access across ASEAN for migrant workers, tourists, and cross-border businesses.

Government Role & CBDC Initiatives

The Bank of Thailand (BOT) advances digital finance through regulatory sandboxes supporting blockchain, AI, and digital asset experimentation. BOT promotes a cloud-first approach for adoption across financial institutions and is piloting a Central Bank Digital Currency (CBDC) to complement PromptPay. Policy direction emphasises open banking frameworks, consumer data rights, and cybersecurity.

The Future of FinTech and Digital Banking in Thailand

Thailand’s financial sector is entering a new phase of digital transformation across the banking sector, shifting from siloed services to open, interoperable ecosystems. Modern digital banking platforms are becoming the foundation for innovation at scale.

AI, Blockchain & Stablecoins

Emerging technologies are shaping digital finance’s future: AI enables hyper-personalised customer journeys and smarter credit scoring, blockchain enhances transparency in cross-border payments and tokenised assets, and stablecoins could lower remittance costs when integrated with regulated frameworks. These innovations are central to bank digital transformation strategy across the region.

Thailand as a Regional FinTech Hub

With regulatory support, technology adoption, and strategic investment, fintech Thailand is positioned as a regional hub. Leadership in QR payments, cross-border interoperability, and real-time settlement makes it a Southeast Asian model [5]. Infrastructure like ITMX, digital bank licences, and CBDC pilots give Thailand tools to expand influence beyond domestic borders, setting standards for digital transformation across ASEAN.

Conclusion & TL;DR

Thailand’s fintech ecosystem has shifted from isolated projects to a connected network of banks, wallets, and startups. Driven by PromptPay, open APIs, and QR payments, the system demonstrates how technology is making financial services faster, more inclusive, and more scalable.

TL;DR:

- Thailand is moving from financial services → ecosystems

- Banks, wallets, and fintech companies are linked via APIs and interoperable payments

- Regulation enables innovation through sandboxes, virtual banks, and CBDC

- Digital banking in Thailand is now the cornerstone of its role as a regional fintech hub

- For international financial institutions, Thailand’s infrastructure maturity and regulatory clarity make it one of the most accessible entry points into Southeast Asian digital finance — but consumer behaviour and trust dynamics require local research before launch

Frequently Asked Questions

What is fintech?

Fintech means using digital tools — apps, AI, and platforms — to make financial services faster, cheaper, and more accessible.

What is digital banking?

Digital banking delivers services like transfers and loans fully online, using modern digital banking platforms available 24/7 without physical branch visits.

What is PromptPay Thailand and how widely is it used?

PromptPay Thailand is the country's flagship instant transfer system with over 77 million registrations, handling up to 75.9 million daily transactions and averaging 538 transactions per person annually.

Which digital wallet is most popular in Thailand?

TrueMoney leads Thailand's digital wallet market with the largest user base, followed by ShopeePay, Rabbit LINE Pay, and SCB Easy, each targeting different user segments and lifestyle needs.

Which digital banks operate in Thailand?

Banks like SCB, Kasikornbank, and Krungsri run digital-first units. The BOT has licensed three new virtual banks, launching by 2026 as fully digital operations.

How is fintech disrupting banking?

By driving API-first systems, cloud platforms, and embedded finance, fintech enables faster innovation and personalised services, fundamentally changing traditional banking models.

References

[1] Statista. “Biggest digital wallet apps on mobile in Thailand as of April 2025.” https://www.statista.com/statistics/1614893/digital-wallet-apps-with-the-highest-mau-in-thailand/

[2] Bank of Thailand. “Cross-border Payment Linkages.” https://www.bot.or.th/en/financial-innovation/digital-finance/digital-payment/cross-border-payment.html

[3] Central Banking. “Thailand approves its first virtual banks.” https://www.centralbanking.com/fintech/7973130/thailand-approves-its-first-virtual-banks

[4] Fintech News Singapore. “New Fintech Thailand Map 2025 Released.” https://fintechnews.sg/111436/thailand/fintech-thailand-map-2025/

[5] Chambers Global Practice Guides. “Fintech 2025 Thailand Overview.” https://practiceguides.chambers.com/practice-guides/fintech-2025/thailand/trends-and-developments

If you wish to quote any information from this article, please kindly cite the source along with the link to the original article to respect copyright. |

Iconic Research Thailand Your trusted partner in market research and consulting across Thailand and Southeast Asia. Headquartered in Bangkok, we provide research-driven insights across the Philippines, Malaysia, Indonesia, Singapore, Laos, and Vietnam. We help businesses navigate Thailand's market complexities through consumer insights, market entry strategy, and trend foresight. Contact us if you have any queries! (+66)888 954 954 |

Contact us

We always looking for new and exciting opportunities. Let’s connect.

Related posts

Brand Strategy: The Decisions That Should Be Built on Evidence

Brand Strategy: The Decisions That Should Be Built on Evidence

Brand strategy is the set of decisions that determine how a brand competes. Those decisions only pay off when they’re built on consumer evidence — not a workshop.

11 min read Key Opinion Leader: What Thai Brands Should Research Before, During, and After a KOL Campaign

Key Opinion Leader: What Thai Brands Should Research Before, During, and After a KOL Campaign

Platform metrics mislead brands choosing and measuring KOLs in Thailand. A research-first look at what to verify before, during, and after a campaign.

10 min read Customer Persona: Build One That Reflects Real Thai Consumers

Customer Persona: Build One That Reflects Real Thai Consumers

Most Thai brands have customer personas built from assumptions. Research-backed personas reveal a different consumer — and drive different decisions.

9 min read