Thailand’s automotive industry is being reshaped by electric vehicle adoption, Chinese brand expansion, and a fundamental shift from price competition to trust-based consumer decisions. Thailand’s position as ASEAN’s largest automotive hub makes it the critical testing ground for how that shift plays out across the region.

Table of Contents

- Thailand as ASEAN’s EV Battleground

- The 2026 Market Structure

- Motor Expo 2025 — When the Trust War Began

- The Energy War — March 2026

- BIMS 2026 — The Trust War Confirmed

- The Manufacturing Collapse

- The Road Ahead — Prognosis

- Winning the Trust War — Iconic Research

- Conclusion

- References

Thailand’s automotive industry is the backbone of the country’s manufacturing economy. The tenth largest vehicle producer globally, it contributes approximately 10–11% of GDP, employs 850,000 people directly, supports a further 1.5 million jobs across more than 2,400 suppliers, and accounts for roughly 12% of Thailand’s total exports. For decades, Thailand earned its reputation as the Detroit of the East — the undisputed automotive manufacturing hub of Southeast Asia.

That industrial foundation is now being restructured faster than at any point in the country’s automotive history. Who makes cars in Thailand, where those cars go, and which brands have committed manufacturing infrastructure versus which arrived only to capture subsidy-driven demand — these are no longer medium-term planning questions. They are being answered now, in real time, across two expos four months apart.

In December 2025, the main question Thai car buyers were asking at Motor Expo was: will this brand still exist in five years? By March 2026, a second question had been added: can I even afford to keep driving petrol?

Four months. Two expos. Three crises hitting simultaneously: a consumer trust war that began in 2024, a fuel price emergency triggered by Middle East conflict, and a structural manufacturing collapse that has been building for two years. Together, they define the state of Thailand’s automotive industry heading into the second half of 2026.

Thailand as ASEAN’s EV Battleground

Thailand is China’s primary Southeast Asian export target — and that position has only hardened as Western tariff walls rise. China broke the 2 million unit export barrier in Q3 2025 alone [1]. For Chinese OEMs locked out of the US and facing rising EU duties, ASEAN is not a secondary market. It is the market. And within ASEAN, Thailand — as the region’s largest automotive industry hub — is the critical testing ground.

China’s investment in Thailand is not only a sales story. BYD’s Rayong manufacturing facility — part of a 30 billion baht commitment across nine projects — represents a direct transfer of production capacity into Thai soil. What looks like market competition at the consumer level is, at the industrial level, a restructuring of who actually builds cars in Thailand.

The Middle East war that began February 28, 2026, and the subsequent disruption to the Strait of Hormuz have now turned Thailand’s oil import dependency into an active vulnerability, accelerating exactly the EV transition China’s OEMs are positioned to supply. The geopolitical and the commercial have converged in ways no market model predicted twelve months ago.

The 2026 Market Structure

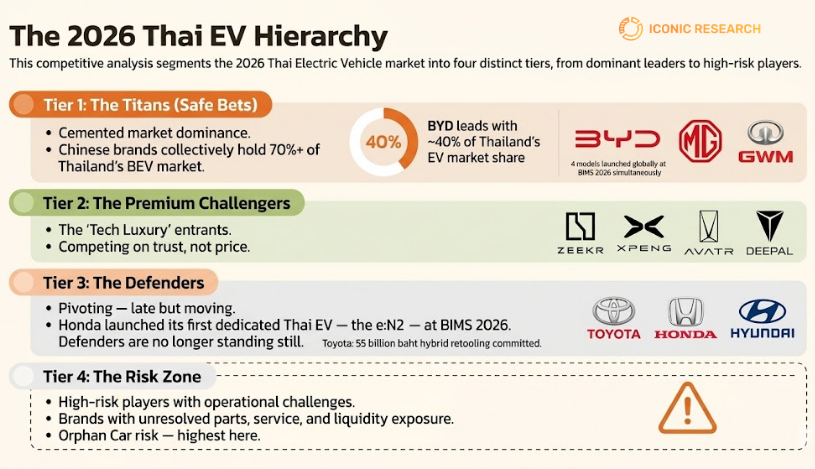

Thailand’s EV market has consolidated around a four-tier hierarchy that was forming in 2024 and is now structural. Within the broader Thailand car market, EVs have shifted from a niche to a contested centre — and the automotive industry in Thailand is being restructured around that shift.

Titans — BYD commands approximately 40% of Thailand’s EV market share. MG and GWM sit behind it, operationally embedded with established dealer networks and parts infrastructure. Chinese brands collectively hold over 70% of Thailand’s BEV market.

Premium Challengers — Zeekr, Xpeng, Avatr, and Deepal are contesting the upper segment, targeting buyers who want Chinese technology without the mass-market associations. Their position depends on trust infrastructure they are still building.

Defenders — Toyota, Honda, and Hyundai remain overall market leaders but have been EV laggards. At BIMS 2026, Honda countered with the e:N2 — its first dedicated EV for the Thai market — a signal that the Defenders are finally moving from ICE defence to EV offence.

Risk Zone — Smaller brands facing liquidity constraints, parts shortages, and shrinking dealer confidence. Several will not survive 2026 in their current form.

The hierarchy maps market position — but it also maps industrial commitment. The Titans are the brands building Thai manufacturing capacity. The Defenders are the brands whose existing plants define Thailand’s industrial identity. The Risk Zone is where brands arrived to capture subsidy demand without building the infrastructure that makes a manufacturer, not just an importer.

Two signals define the current moment. BYD simultaneously launched four new models at BIMS 2026 — Atto 1, Atto 2, Seal 6, and Sealion 5 DM-i — the first time any brand has debuted four vehicles at a single Thailand event. A brand that does that is treating Thailand as a primary market, not an export afterthought. Geely’s EX2 at THB 400,000 represents a new affordability threshold that could materially change the EV buyer profile if trust conditions permit.

Motor Expo 2025 — When the Trust War Began

Motor Expo 2025 (November 28 – December 11, 2025) closed with 80,509 total bookings — 75,246 cars and 5,263 motorcycles — against 1.52 million visitors. On paper, a boom. In reality, borrowed demand: the 150,000 THB government EV subsidy expired December 31st, and buyers were racing to beat the deadline. Toyota led with 10,872 bookings, followed by Honda (6,267) and BYD (6,212). EVs accounted for exactly 50% of car bookings.

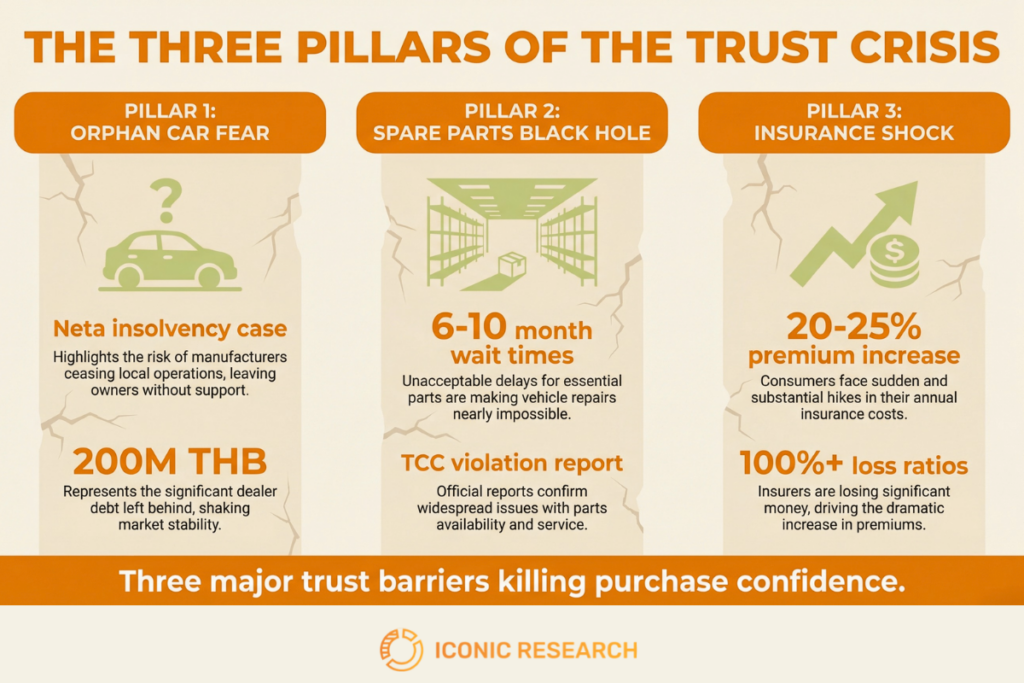

What the booking numbers did not show was the mood on the floor. Three trust crises had been building throughout 2024–2025.

The Orphan Car Fear. Neta Auto’s parent company collapse in China — 18 Thai dealers filing complaints over 200 million THB in unpaid debts — had planted a simple, rational fear: what if my brand disappears? Buyers were no longer just reading specifications. They were reading balance sheets.

The Spare Parts Black Hole. Thailand’s Consumer Council flagged parts shortages as a critical rights violation in 2025. EV owners waiting 6–10 months for collision repairs. The “cheap running costs” argument was hollow if the car sat unrepaired for most of the year.

The Insurance Shock. EV insurance premiums in Thailand rose 20–25% in 2025, with some insurers recording loss ratios above 100% and refusing to cover certain brands entirely [2].

The Energy War — March 2026

On February 28, 2026, the United States and Israel struck Iran. Within days, the Strait of Hormuz — through which a significant portion of Thailand’s crude oil passes — was disrupted. Thailand’s Oil Fuel Fund, already carrying a 50+ billion baht deficit from previous crises, began absorbing a subsidy burden of over 1.7 billion baht per day.

On March 25, 2026 — the same morning the Bangkok International Motor Show opened its doors — pump prices rose 6 baht per litre overnight. Midnight queues formed at petrol stations. The government confirmed Thailand had roughly 39 days of fuel reserves. By April 5, diesel reached a historic high of 50.54 baht per litre.

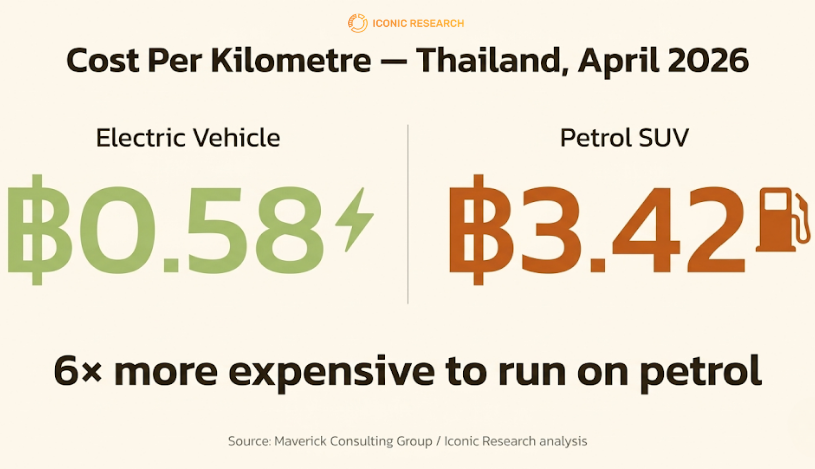

The arithmetic of EV ownership became viscerally clear overnight: approximately 0.58 baht per kilometre for an EV against 3.42 baht per kilometre for a comparable petrol SUV. A sixfold difference, suddenly and painfully visible at every petrol station.

Prime Minister Anutin drove a BYD Sealion 7 to Government House for three consecutive days. No motorcade. A deliberate signal to three audiences: consumers, investors, and the world.

But the same energy shock that made EVs appealing was destroying the purchasing power needed to buy them. A 1.2 million baht entry-level EV is no answer to a family whose logistics costs have just spiked.

BIMS 2026 — The Trust War Confirmed

The Bangkok International Motor Show 2026 (March 25 – April 5) opened in this context. By the midpoint of the event, bookings had reached 41,778 units — a 68.8% increase over the equivalent point in BIMS 2025, which closed at 79,941 total.

The floor told a more nuanced story than the numbers. EV displays drew heavy crowds, driven by fuel-shock urgency. The Thailand EV market had never been more visible — or more anxious. But the brands responding most effectively were not fighting on price — they were fighting on trust.

BYD launched a “Lifetime Warranty” campaign exclusively for Motor Show buyers. Not a price cut. A commitment. Exactly the Trust War playbook.

New entrants kept arriving despite the consolidation signals: Firefly (BYD’s new budget sub-brand), Forthing, and Lepas joined the show for the first time, bringing total Chinese OEM presence to 17 brands. The wave has not reversed.

The two-wheeler hall told a different story: petrol motorcycles dominated, electric models were subdued. In a lower ticket-size category where switching costs are smaller, Thai consumers showed more caution about EV brands, not less. Trust travels slowly at every price point.

The Manufacturing Collapse

The BOI’s 2:1 local production requirement — produce two Thai-assembled vehicles for every one imported — came into full effect in 2026. It is already sorting serious players from short-term entrants.

The wider manufacturing picture is stark. Subaru has closed its Bangkok plant. Suzuki has announced closure of its Rayong facility. Honda has halved production capacity. Nissan has shut one of its two Thai factories. Isuzu remains a significant exception — its Thai manufacturing base and dominance in the pickup segment give it structural insulation the passenger car brands lack.

Total vehicle production fell approximately 20% in 2024 to around 1.5 million units — 18 consecutive months of decline through early 2025 [3]. The Krungthai COMPASS report estimates over 100,000 auto workers face redundancy between 2025 and 2026. As a share of GDP, the contraction hitting the Thai automotive industry is the most significant structural shock since 1997.

The Thailand automotive industry’s response has been uneven.

Toyota’s response has been strategically distinct: a 55 billion baht commitment to retool Thai production lines for hybrid vehicles, with Chairman Akio Toyoda delivering the pledge personally to the Prime Minister. A long-term bet, not a retreat.

The Road Ahead — Prognosis

The Electric Vehicle Association of Thailand projects over 120,000 BEVs sold in 2026 [4]. The Thailand electric vehicle market is reaching that number faster than forecast — the oil shock has compressed a multi-year adoption curve into months.

The projection carries a caveat. If Brent crude stabilises at $85–95 per barrel in H2 2026, the cost-per-kilometre calculation that made EVs compelling loses its urgency. The December 2025 subsidy expiry already produced a wave of front-loaded purchases. The oil shock may be producing a second. Both waves generate bookings that look like structural growth but reflect pulled-forward demand. On the production side, the Federation of Thai Industries projects 1.5 million total units in 2026 — 950,000 for export — but whether that export target is achievable depends on which manufacturers still have functioning Thai capacity after the consolidation completes.

What remains when the urgency recedes is the Trust War. Parts availability, insurance coverage, resale value, and brand continuity are the variables that determine purchase decisions when price is no longer the driver. Thailand’s automotive industry research agenda for H2 2026 is straightforward: measure trust, not intention.

Winning the Trust War — Iconic Research

Case Study 1: Premium EV Value Perception. Conjoint analysis revealed that Thai luxury EV buyers prioritise resale guarantees and service network depth over hardware specifications — a finding that reordered product launch priorities for one OEM client. Read the case study.

Case Study 2: B-MPV ASEAN Feature Localisation. Ethnographic research across Thai households identified which features were locally decisive and which were over-engineered for the market — preventing a wrong-feature launch that would have cost significantly more than the research. Read the case study.

Case Study 3: Chinese EV Perception Across Five ASEAN Markets. Research across Thailand, Indonesia, Vietnam, the Philippines, and Malaysia found that Chinese EV brands are perceived as technology leaders, not budget alternatives — a positioning gap that incumbent brands have consistently underestimated. Read the case study.

If your brand is navigating the Thai EV market, our car clinic and automotive research services are the starting point.

Conclusion

The Gold Rush era is over. 2026 is the consolidation year, complicated by an energy shock that accelerated the EV timeline without solving the trust problem. The brands that treat trust as an operational commitment — not a campaign — will survive it. Those that arrived to capture subsidy-driven volume without building service infrastructure will not.

Thailand’s automotive industry will exit 2026 smaller, less diverse, and more competitive. For brands that have done the research, that is an opportunity.

Frequently Asked Questions

Which brands are committed to local manufacturing in Thailand?

BYD, MG, GWM, and Changan have operational or planned local assembly commitments meeting the BOI's 2:1 requirement. Hyundai has confirmed manufacturing plans. Toyota has made the largest incumbent bet — 55 billion baht to retool Thai lines for hybrid production.

What is driving the manufacturing contraction in Thailand's automotive industry?

Three forces: the BOI 2:1 requirement forcing brands without genuine assembly commitment to exit; Chinese EVs displacing ICE volume that sustained Japanese operations; and falling ICE demand making existing plant capacity unviable. Subaru, Suzuki, and Nissan have closed facilities. Honda has halved capacity. Production fell approximately 20% in 2024.

How does the oil price shock affect EV adoption in Thailand?

Diesel reached 50.54 baht per litre in early April, making the cost gap — 0.58 baht per kilometre for EVs versus 3.42 baht for a comparable petrol SUV — impossible to ignore. BIMS bookings rose 68.8% over the prior year. The risk is pulled-forward demand: if energy prices stabilise in H2 2026, urgency recedes and trust barriers reassert as the primary constraint.

What are the key trust barriers in Thailand's EV segment?

Three structural barriers: the Orphan Car Fear (brand viability uncertainty after Neta's collapse), the Spare Parts Black Hole (6–10 month repair waits), and the Insurance Shock (premiums up 20–25% in 2025, some insurers refusing coverage entirely).

How should brands approach the 2026 Trust War?

Operationally, not communicationally. Parts inventory depth, service network coverage outside Bangkok, and resale value guarantees backed by buy-back programmes are the variables that matter. Research measuring verified consumer perception — not brand-commissioned surveys — identifies where trust gaps actually sit.

References

[1] PwC Strategy& (2025). China Automotive Export Analysis Q3 2025. https://www.strategyand.pwc.com

[2] Office of the Insurance Commission, Thailand (2025). EV Insurance Market Report. OIC. https://www.oic.or.th

[3] Federation of Thai Industries, Automotive Industry Club (2025). Thailand Automotive Production Statistics 2024. FTI. https://www.thaiauto.or.th

[4] Electric Vehicle Association of Thailand (2026). Thailand EV Market Outlook 2026. EVAT. https://www.evat.or.th

[5] Krungthai COMPASS (2025). Thailand Automotive Industry Labour Impact Assessment. Krungthai Bank. https://krungthai.com/th/krungthai-update/research-detail/530

If you wish to quote any information from this article, please kindly cite the source along with the link to the original article to respect copyright. |

Iconic Research Thailand Your trusted partner in market research and consulting across Thailand and Southeast Asia. Headquartered in Bangkok, we provide research-driven insights across the Philippines, Malaysia, Indonesia, Singapore, Laos, and Vietnam. We help businesses navigate Thailand's market complexities through consumer insights, market entry strategy, and trend foresight. Contact us if you have any queries! (+66)888 954 954 |

Contact us

We always looking for new and exciting opportunities. Let’s connect.

Related posts

Growth Strategy: The Expansion Decisions That Need Evidence

Growth Strategy: The Expansion Decisions That Need Evidence

Growth strategy is the set of decisions about where a company expands next. Only 25% of companies grow sustainably — the difference is evidence, not ambition.

9 min read Brand Strategy: The Decisions That Should Be Built on Evidence

Brand Strategy: The Decisions That Should Be Built on Evidence

Brand strategy is the set of decisions that determine how a brand competes. Those decisions only pay off when they’re built on consumer evidence — not a workshop.

11 min read Key Opinion Leader: What Thai Brands Should Research Before, During, and After a KOL Campaign

Key Opinion Leader: What Thai Brands Should Research Before, During, and After a KOL Campaign

Platform metrics mislead brands choosing and measuring KOLs in Thailand. A research-first look at what to verify before, during, and after a campaign.

10 min read