Philippines Market Research: What the English-Speaking Surface Doesn’t Tell You

10 min readPhilippines market research starts with a market international businesses consistently misread — not because it is opaque, but because it appears familiar. The Philippines is Southeast Asia’s most English-fluent consumer market, and the one most often entered on untested assumptions as a result. 113 million people across 7,600 islands, with consumption patterns shaped by remittances, BPO income, and strong regional identity. If it looks like a Western market, it researches like one. It does not.

Table of Contents

- The Philippines at a Glance

- The Philippine Consumer

- What Western Assumptions Get Wrong

- Key Research Considerations for the Philippines

- Working with a Research Partner for the Philippines

- References

English is everywhere. The population is young and digitally connected. Global brands are visible. This article covers what philippines market research actually involves at the market entry stage — what the market looks like, where familiar-looking surfaces produce unfamiliar results, and what research is required before a brief is written.

The Philippines at a Glance

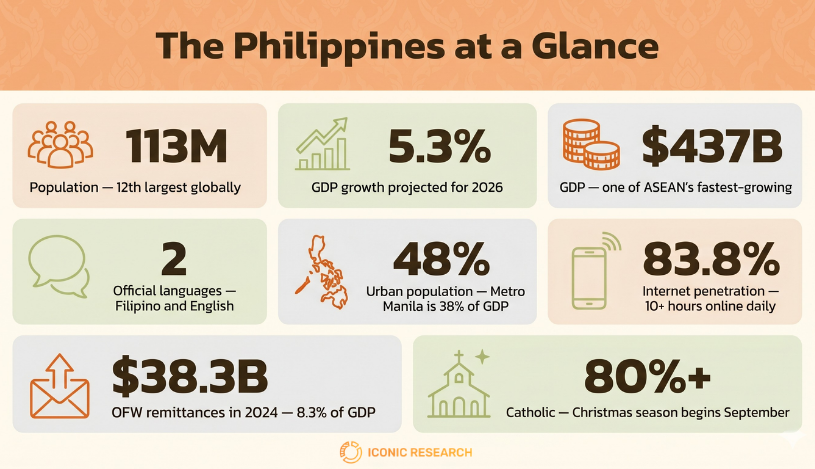

Facts only [1][2]:

- Population: 113 million. Twelfth largest globally.

- GDP: approximately $437 billion. One of ASEAN’s fastest-growing economies — GDP growth projected to recover to 5.3% in 2026 [2].

- Official languages: Filipino and English. English proficiency among the highest in Asia — research instruments do not require translation for urban samples.

- Urban-rural split: approximately 48% urban, rising. Metro Manila accounts for roughly 38% of GDP but is not representative of the broader market.

- Digital penetration: 97.5 million internet users, 83.8% of the population [3]. Social media usage among the highest globally — average Filipino spends over 10 hours online daily.

- Remittances: $38.34 billion in 2024 — a record high, equivalent to approximately 8.3% of GDP [4]. OFW money drives provincial consumption in ways not visible in standard income data.

- Key economic sectors: BPO and services, remittance-driven consumer goods, FMCG, real estate, tourism, infrastructure, and renewable energy.

- Religion: 80%+ Catholic. The Christmas season begins in September — the single largest retail consumption event of the year.

The Philippine Consumer

Philippines market research begins with understanding philippines consumer behavior — this is not one consumer market but several, separated by geography, income source, and cultural identity.

Luzon, Visayas, Mindanao — Not One Market

The Philippines is an archipelago of 7,600 islands grouped into three major island groups. Consumer behaviour, brand familiarity, income levels, and channel preference differ significantly between Metro Manila, provincial Luzon, the Visayas, and Mindanao. Research scoped to Metro Manila produces Metro Manila data — and Metro Manila is not the Philippines.

The OFW Economy

Approximately 1.96 million Filipinos were working overseas as of 2023 [1], sending home $38.34 billion annually [4]. These remittances flow disproportionately to provincial households, funding consumption that does not appear in formal income data. Families in Cebu or Iloilo with an OFW member have meaningfully different purchasing power and aspiration profiles than their income tier would suggest. Research that does not account for remittance income systematically underestimates provincial purchasing power. See fieldwork and recruitment for how sampling design accounts for income variation across geographic zones [5].

English Proficiency and Research Design

The Philippines is the only ASEAN market where research instruments can run in English across most urban demographics without translation. This reduces instrument design complexity and enables direct comparison with other English-language markets. It also creates a trap: English fluency is not cultural equivalence. Filipino consumer decision-making is shaped by family structures, social values, and peer dynamics that require cultural fluency, not just linguistic access.

Generational Dynamics

Median age: 24.1 years — among the youngest in ASEAN. Gen Z and millennials dominate consumption. They are heavily influenced by Filipino content creators, local KOLs, and peer recommendation on TikTok, Facebook, and YouTube. Global brand advertising without local influencer integration consistently underperforms against domestically produced content at a fraction of the budget.

The Catholic Consumption Calendar

Christmas in the Philippines begins in September — the so-called “Ber months.” By October, retail is in full seasonal mode. This is the single largest consumption event in the market and reshapes FMCG, retail, electronics, and financial services planning for the entire second half of the year. Research that does not account for this calendar produces forecasts that misread seasonal volume.

What Western Assumptions Get Wrong

The English Assumption

English fluency does not mean Western consumer behaviour. Filipino purchasing decisions are heavily influenced by family consensus, brand trust built through community endorsement, and a strong preference for locally familiar brands in certain categories. A foreign brand entering on the assumption that English-language global creative will land is entering on an untested hypothesis.

The Metro Manila Assumption

Metro Manila is visible, accessible, and measurable. It is also not representative. Provincial Philippines — which accounts for the majority of the population — has different income profiles, different channel structures, and different brand relationships. FMCG brands that validate in Manila and roll out nationally consistently find their provincial performance diverges from the Manila signal.

The Digital Engagement Assumption

The Philippines has some of the highest social media usage rates globally [3]. This does not translate directly to e-commerce conversion — Philippines ecommerce penetration remains lower than digital engagement suggests, particularly outside Metro Manila where logistics infrastructure limits last-mile delivery. Research that equates social engagement with purchase intent produces forecasts that overestimate online channel volume.

The Income Data Assumption

Standard income data misses remittance flows. A household classified as lower-middle income in national statistics may have OFW income that puts actual spending power significantly higher. Market sizing based on formal income data without remittance adjustment underestimates addressable market in provincial Philippines.

Key Research Considerations for the Philippines

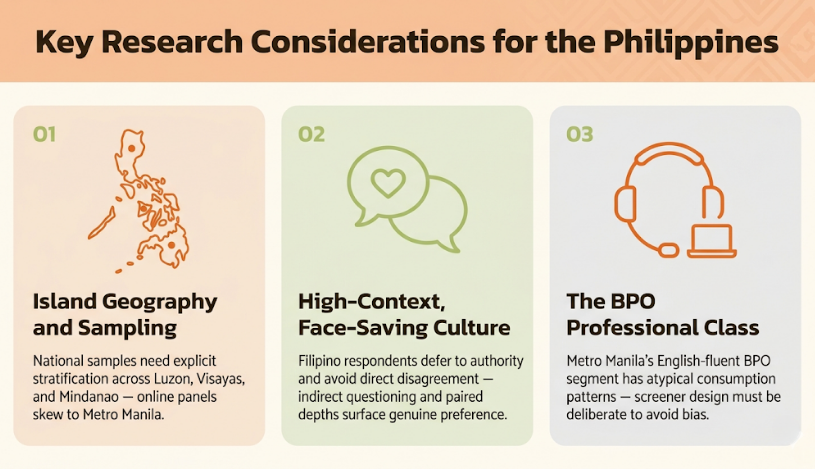

Island Geography and Sampling

A nationally representative sample requires explicit geographic stratification across Luzon, Visayas, and Mindanao. Online panels skew toward Metro Manila and urban Luzon. Research designs that default to panel convenience produce findings that represent Metro Manila demographics at national scale — a common and expensive error. Quantitative research for the Philippines requires explicit sampling strategy across geographic zones. Defining which audience segment is being researched before the sampling frame is built is the prerequisite — see target audience for the methodology.

Qualitative in a High-Context, Face-Saving Culture

Filipino respondents are highly socially oriented in research settings. Agreement with moderator positions, reluctance to express negative opinions directly, and deference to perceived authority figures in group settings all suppress honest feedback in standard focus group designs. Skilled qualitative research design uses indirect questioning, projective techniques, and paired depth interviews to surface genuine preference rather than socially acceptable response.

The BPO Professional Class

Metro Manila has a large, English-fluent, internationally oriented professional class employed in BPO and shared services. This segment has consumption patterns, aspirations, and brand relationships that differ significantly from the broader Filipino population. Research that recruits from this segment without deliberate screener design ends up studying a highly atypical demographic.

Multi-Country Coordination

For international businesses entering the Philippines as part of a broader ASEAN rollout, the research coordination challenge mirrors Indonesia — parallel programmes through separate local agencies produce inconsistent methodologies and incomparable findings. Iconic Research coordinates Philippines market research through established long-term fieldwork partnerships, running unified research programmes from Bangkok across multiple ASEAN markets simultaneously.

In practice, this means projects like a four-market automotive feature development programme that included the Philippines — recruiting B-MPV dealers and end users across the Philippines, Vietnam, Malaysia, and Thailand, managing bilingual fieldwork, and delivering unified findings to an international automotive client. See case study.

Scoping a Philippines market entry — or a broader ASEAN rollout? Research design starts before the business case. Talk to our team about how we coordinate multi-country research programmes.

Working with a Research Partner for the Philippines

International businesses entering the Philippines need a research partner who understands both the brief and the market. The relevant questions: Does the agency have fieldwork capability outside Metro Manila? Do they understand the OFW income dynamic and how to account for it in sampling? Can they design qualitative research that surfaces genuine preference rather than socially acceptable response?

Iconic Research coordinates Philippines market research and international market research programmes through established long-term fieldwork partnerships across Luzon, Visayas, and Mindanao. Research is designed from Bangkok, executed in-country, and delivered as unified findings — whether the Philippines is the sole market or one of several running in parallel. See fieldwork and recruitment for how we structure in-country execution.

For clients who have entered Thailand first and are expanding the ASEAN footprint, the research model is consistent — same methodology, same quality standards, different market. See market entry Thailand for the reference model. One consideration unique to the Philippines: the BPO professional class in Metro Manila is a distinct research population that requires deliberate screener design to avoid skewing findings toward an atypical, internationally oriented demographic. For a comparable briefing on the region’s largest market, see Indonesia market research.

Frequently Asked Questions

What does market research in the Philippines involve?

Consumer landscape research accounting for remittance income, island geography, and generational dynamics. Segmentation to identify which audience is most accessible. Product or concept testing with real Filipino consumers. Distribution research across modern trade in Metro Manila versus sari-sari stores and provincial channels.

How is the Philippines different from other ASEAN markets to research?

English proficiency removes the translation barrier but not the cultural one. OFW remittances create purchasing power that standard income data misses. Island geography requires deliberate sampling across three major island groups. A face-saving research culture requires qualitative design that goes beyond standard focus groups.

What does doing business in Philippines require from a research perspective?

Understanding which Philippines you are entering — Metro Manila's professional class, provincial markets shaped by remittances, or the archipelago as a whole. Each has a different research brief and a different competitive landscape.

Does Iconic Research conduct fieldwork in the Philippines?

Yes — through established long-term partnerships across Metro Manila and provincial markets, in English and Filipino, with quality control from the Bangkok team. Philippines fieldwork has run as part of multi-country ASEAN programmes including a four-market automotive project across the Philippines, Vietnam, Malaysia, and Thailand.

What sectors does Iconic Research cover in the Philippines?

FMCG, automotive, healthcare and pharmaceuticals, financial services, technology and digital products, and market entry for international brands. Each sector has different research requirements and we scope accordingly.

References

[1] Philippine Statistics Authority. Population and Housing. https://www.psa.gov.ph

[2] World Bank (December 2025). Philippines Economic Update — Growth Corridors: Pathways Out of Poverty. https://www.worldbank.org/en/country/philippines/publication/philippine-economic-updates

[3] We Are Social / Meltwater (2025). Digital 2025: Philippines. https://datareportal.com/reports/digital-2025-philippines

[4] Bangko Sentral ng Pilipinas (2025). Selected Economic and Financial Indicators. https://www.bsp.gov.ph/statistics/keystat/sefi.pdf

[5] Iconic Research (2026). Fieldwork and Research Recruitment. https://iconicthai.com/services/fieldwork/

If you wish to quote any information from this article, please kindly cite the source along with the link to the original article to respect copyright. |

Iconic Research Thailand Your trusted partner in market research and consulting across Thailand and Southeast Asia. Headquartered in Bangkok, we provide research-driven insights across the Philippines, Malaysia, Indonesia, Singapore, Laos, and Vietnam. We help businesses navigate Thailand's market complexities through consumer insights, market entry strategy, and trend foresight. Contact us if you have any queries! (+66)888 954 954 |

Contact us

We always looking for new and exciting opportunities. Let’s connect.

Related posts

Growth Strategy: The Expansion Decisions That Need Evidence

Growth Strategy: The Expansion Decisions That Need Evidence

Growth strategy is the set of decisions about where a company expands next. Only 25% of companies grow sustainably — the difference is evidence, not ambition.

9 min read Brand Strategy: The Decisions That Should Be Built on Evidence

Brand Strategy: The Decisions That Should Be Built on Evidence

Brand strategy is the set of decisions that determine how a brand competes. Those decisions only pay off when they’re built on consumer evidence — not a workshop.

11 min read Key Opinion Leader: What Thai Brands Should Research Before, During, and After a KOL Campaign

Key Opinion Leader: What Thai Brands Should Research Before, During, and After a KOL Campaign

Platform metrics mislead brands choosing and measuring KOLs in Thailand. A research-first look at what to verify before, during, and after a campaign.

10 min read