FMCG Industry in Thailand: Growth, Trends, and Digital Transformation

10 min readFMCG — fast-moving consumer goods — encompasses the packaged foods, beverages, personal care, and household products that Thai consumers purchase repeatedly and in high volume. Thailand’s FMCG industry is one of Southeast Asia’s most competitive and digitally advanced, shaped by a retail infrastructure that runs from 7-Eleven to TikTok Shop, and by FMCG companies ranging from CP Group and ThaiBev to Unilever and P&G.

Table of Contents

- Introduction: The Changing Face of FMCG in ASEAN and Thailand

- What Defines the FMCG Industry

- FMCG in Thailand: Market Landscape and Leading Players

- Digital Transformation in FMCG: Data and E-Commerce

- Opportunities and Challenges Ahead

- Market Research in FMCG: The Thai Context

- Conclusion

- References

Introduction: The Changing Face of FMCG in ASEAN and Thailand

Across ASEAN, the FMCG industry is evolving rapidly. With a combined population exceeding 680 million and a growing middle class, Southeast Asia has become one of the world’s most promising consumer markets. Thailand, Vietnam, and Indonesia are leading this transformation through digitalization, infrastructure development, and shifting consumer preferences [1][5].

In Thailand, the FMCG industry plays a particularly strategic role at the crossroads of regional manufacturing, retail distribution, and export trade. Thai consumers are tech-savvy and increasingly values-driven—demanding products that align with sustainability, wellness, and affordability. From 7-Eleven’s convenience retail dominance to the rise of Shopee and LINE SHOPPING for grocery delivery, FMCG Thailand reflects a unique blend of online and offline integration.

This transformation has created an FMCG landscape defined by speed, data, and digital inclusion. Whether through AI-powered retail analytics, cross-border e-commerce, or eco-conscious packaging, FMCG companies in Thailand are setting regional benchmarks for innovation and consumer engagement [6].

What Defines the FMCG Industry

The FMCG meaning centers on goods with a short shelf life that are sold quickly at relatively low prices, creating high-volume turnover that drives retail economics. Core FMCG products include:

Food & Beverages: Snacks, ready-to-drink products, instant meals that consumers purchase frequently

Personal Care & Cosmetics: Skincare, toiletries, haircare products that represent daily necessities

Household Products: Detergents, cleaners, paper goods essential for home maintenance

OTC Health Products: Vitamins and supplements that bridge healthcare and consumer goods

While closely related, FMCG and CPG (Consumer Packaged Goods) differ slightly—FMCG emphasizes rapid consumption and volume turnover, whereas CPG can include durable items like pet supplies or home essentials with longer lifecycles [2]. Understanding this distinction helps businesses position products appropriately within distribution channels.

This segmentation underscores the diversity of FMCG and its pervasive influence across daily life, touching virtually every household multiple times per day.

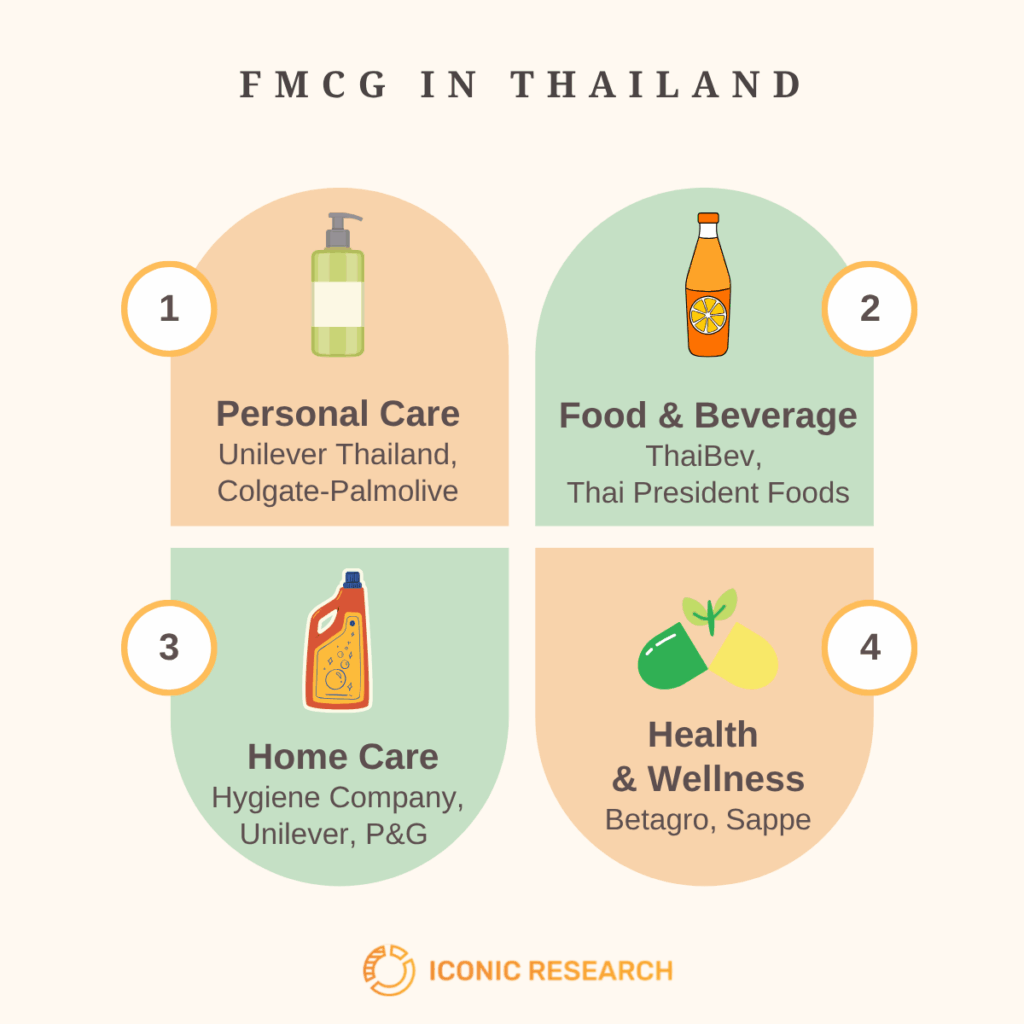

FMCG in Thailand: Market Landscape and Leading Players

Thailand’s FMCG market is one of the largest and most competitive in Southeast Asia. According to Worldpanel by Numerator, the country’s FMCG sector grew by over 6% in 2024, driven by strong demand in food, beverage, and personal care categories [5]. Urbanization, rising incomes, and the recovery of international tourism are fueling consumption both in modern trade outlets and online platforms.

Leading FMCG companies in Thailand include global giants like Unilever, P&G, ThaiBev, Osotspa, Betagro, and Sappe, alongside powerful domestic conglomerates like CP Group and Malee. These companies compete not just on product quality but on distribution reach and brand loyalty. FMCG distributors in Thailand such as Berli Jucker and DKSH Thailand serve as critical intermediaries that ensure product reach across thousands of convenience stores, FMCG store locations, and retail points nationwide—making distribution capability as important as product innovation.

Thailand’s strong logistics network and strategic geographic location make it a regional FMCG hub, serving neighboring ASEAN markets such as Cambodia, Laos, and Vietnam. Yet, rising operational costs and intense competition from both multinational and local brands require companies to continually innovate, localize, and differentiate to sustain growth [6]. Success increasingly depends on understanding hyper-local preferences while maintaining the operational efficiency that FMCG demands.

For FMCG brands tracking whether these research interventions are translating into retained customers, our guide to customer satisfaction measurement covers how to run CSAT and NPS programmes correctly in Thailand — including why Thai-market baselines matter more than global benchmarks.

Digital Transformation in FMCG: Data and E-Commerce

The FMCG industry in 2025 is undergoing a digital revolution that fundamentally reshapes how products are produced, marketed, and delivered. In Thailand, three major drivers—Big Data, E-commerce, and new digital verticals—are transforming traditional business models that have defined the industry for decades.

Data-Driven Decision-Making

Big Data FMCG represents one of the most significant shifts in how companies operate. Big data in FMCG allows brands to forecast demand, personalize marketing, and optimize supply chains with unprecedented precision. Through AI and predictive analytics, companies can analyze purchasing behavior and social sentiment in real time, responding to market shifts within hours rather than weeks.

Thai FMCG manufacturers increasingly rely on data partnerships between retailers and producers to manage promotions and reduce waste [3][6]. By integrating data from loyalty programs, sales platforms, and logistics systems, brands achieve higher forecasting accuracy and faster time-to-market. This data-centric approach transforms FMCG from a volume game into a precision business where insights drive every decision from product development to shelf placement.

E-Commerce and Omnichannel Expansion

FMCG ecommerce has redefined how Thai consumers shop for fast-moving goods, fundamentally altering the competitive landscape. Platforms like Shopee, Lazada, LINE SHOPPING, and TikTok Shop now account for a growing share of grocery, beauty, and household sales. This trend, accelerated by mobile-first adoption, has also empowered micro-retailers and local brands to compete through digital storefronts and social commerce [2][4].

In response, large FMCG companies have adopted omnichannel strategies—linking offline stores, online marketplaces, and direct-to-consumer websites. This integration provides convenience, real-time inventory updates, and personalized offers, aligning with the expectations of Thailand’s increasingly connected consumers who often research products online before purchasing in physical stores, or vice versa.

Opportunities and Challenges Ahead

Thailand’s FMCG sector offers immense potential, but navigating it successfully requires addressing critical challenges while capitalizing on emerging opportunities.

Challenge | Impact | Opportunity / Strategic Value |

Rising Costs | Supply chain and currency fluctuations increase production and logistics expenses. | Use AI-driven analytics to optimize supply chains and forecast demand. |

Sustainability Pressure | Regulators demand eco-friendly packaging and ethical sourcing. | Develop green product lines and sustainable packaging. |

Hypercompetition | Local and global brands compete for price-sensitive shoppers; loyalty is fragile. | Differentiate through branding, data-driven marketing, and emotional engagement. |

Cross-Border Trade | ASEAN integration opens new regional markets but increases competitive exposure. | Expand distribution networks and leverage regional trade to capture growth. |

The winners will be those who can balance efficiency with innovation, and scale with sustainability—using data intelligence and regional integration to build resilience while addressing cost pressures and evolving consumer expectations.

Market Research in FMCG: The Thai Context

In Thailand’s dynamic FMCG landscape, market research has become indispensable for brands navigating rapid digital transformation and evolving consumer preferences. Effective FMCG market research requires understanding both quantitative metrics and qualitative cultural nuances—revealing not just what Thai customers buy, but why they choose one brand over another and how regional preferences differ between Bangkok and provincial markets.

FMCG research in Thailand draws on a specific set of methods suited to high-frequency, low-involvement purchase categories. Central Location Tests (CLTs) place product stimuli in front of recruited respondents for blind or branded taste tests, pack evaluations, and concept assessments — the standard for new product development across food, beverage, and personal care.

Accompanied shopping studies track how consumers navigate retail aisles, respond to promotions, and make purchase decisions in real environments, capturing behaviour that recall surveys miss.

Social listening monitors brand and category mentions across Pantip, TikTok, and Facebook in real time, identifying emerging trends and product complaints before they reach category review cycles.

And pricing research — conjoint analysis and van Westendorp studies — establishes acceptable price ranges in a market where Thai consumers are value-conscious and promotional sensitivity is high.

For a full breakdown of how these methods are designed and executed — including blind vs branded test protocols, monadic design, and IHUT logistics in Thailand — see our product testing guide.

Conclusion

The FMCG industry is being redefined by speed, data, and digital integration. Brands can no longer depend on mass marketing alone—they must embrace predictive analytics, agile product cycles, and customer-centric experiences that respond to real-time market signals.

In Thailand and across ASEAN, FMCG growth increasingly depends on a brand’s ability to connect digital intelligence with local culture. Those who combine automation, data insights, and sustainability will not only thrive domestically but position themselves as regional leaders in the next generation of consumer innovation [5][6]. The FMCG companies that succeed will be those that recognize their products may be fast-moving, but their strategies must be even faster.

Frequently Asked Questions

What does FMCG stand for?

Fast-Moving Consumer Goods—everyday items like food, drinks, toiletries, and household products that sell quickly at low prices.

What is the FMCG industry?

It includes companies that produce and distribute high-turnover consumer products with short shelf lives and frequent repeat purchases.

Who are the major FMCG companies in Thailand?

Leading players include Unilever, P&G, CP Group, ThaiBev, Osotspa, Sappe, Betagro, and major distributors like Berli Jucker and DKSH.

How is digital transformation shaping FMCG in Thailand?

It fuels ecommerce growth, improves demand forecasting through big data analytics, and strengthens omnichannel retail integration.

What’s the difference between FMCG and CPG?

FMCG focuses on fast-selling, frequently purchased goods, while CPG covers both fast-moving items and longer-lasting consumer products.

What is the FMCG meaning in business?

FMCG meaning in business refers to the category of fast-moving consumer goods — products with a short shelf life, high purchase frequency, and relatively low unit price. The term distinguishes these high-velocity categories (packaged food, beverages, personal care, household goods) from durable goods and slow-moving categories. In Thailand, FMCG companies operate across modern trade, traditional trade, and a rapidly growing e-commerce channel.

References

[1] McKinsey & Company. “State of the Consumer Trends Report 2025.” https://www.mckinsey.com/industries/consumer-packaged-goods/our-insights/state-of-consumer

[2] Food & Hotel Asia. “Understanding the FMCG Sector in 2025: Key Trends and Market Insights.” https://www.foodnhotelasia.com/blog/fnb/understanding-the-fmcg-sector/

[3] Deep Market Insights. “Global FMCG Market Size & Outlook, 2025-2033.” https://deepmarketinsights.com/vista/insights/fmcg-market/global

[4] MarketReportsWorld. “FMCG (Fast-Moving Consumer Goods) Market Size, Share, Growth, and Industry Analysis.” https://www.marketreportsworld.com/market-reports/fmcg-fast-moving-consumer-goods-market-14720327

[5] Worldpanel by Numerator. “2024 Thailand FMCG Outlook Report.” https://market.worldpanelbynumerator.com/th/news/2024-Thailand-FMCG-Outlook-Report

[6] DDX Transformation Insights. “Digital Transformation Meets the Rising Tide of Out-of-Home Consumption in Thailand.” https://insights.ddxtransformation.com/insights/digital-transformation-meets-the-rising-tide-of-out-of-home-consumption-in-thailand

If you wish to quote any information from this article, please kindly cite the source along with the link to the original article to respect copyright. |

Iconic Research Thailand Your trusted partner in market research and consulting across Thailand and Southeast Asia. Headquartered in Bangkok, we provide research-driven insights across the Philippines, Malaysia, Indonesia, Singapore, Laos, and Vietnam. We help businesses navigate Thailand's market complexities through consumer insights, market entry strategy, and trend foresight. Contact us if you have any queries! (+66)888 954 954 |

Contact us

We always looking for new and exciting opportunities. Let’s connect.

Related posts

Growth Strategy: The Expansion Decisions That Need Evidence

Growth Strategy: The Expansion Decisions That Need Evidence

Growth strategy is the set of decisions about where a company expands next. Only 25% of companies grow sustainably — the difference is evidence, not ambition.

9 min read Brand Strategy: The Decisions That Should Be Built on Evidence

Brand Strategy: The Decisions That Should Be Built on Evidence

Brand strategy is the set of decisions that determine how a brand competes. Those decisions only pay off when they’re built on consumer evidence — not a workshop.

11 min read Key Opinion Leader: What Thai Brands Should Research Before, During, and After a KOL Campaign

Key Opinion Leader: What Thai Brands Should Research Before, During, and After a KOL Campaign

Platform metrics mislead brands choosing and measuring KOLs in Thailand. A research-first look at what to verify before, during, and after a campaign.

10 min read