Vietnam Market Research: The Market Behind the Manufacturing Story

10 min readVietnam market research has changed brief. Vietnam is no longer just a manufacturing destination. With 8% GDP growth in 2025, a $514 billion economy, and 101 million people mid-transition from production economy to consumer market, international businesses that arrive with a supply chain strategy and leave without a consumer research programme are missing the market their own factories are helping to create.

Table of Contents

- Vietnam at a Glance

- The Vietnamese Consumer

- What the Manufacturing Brief Misses

- Key Research Considerations for Vietnam

- Working with a Research Partner for Vietnam

- References

The dominant narrative about the Vietnam market is Vietnam manufacturing — China plus one, supply chain diversification, FDI inflows at a five-year high of $27.6 billion disbursed in 2025 [1]. That narrative is accurate and it is incomplete. Every factory that moves to Vietnam brings with it an international business that will, eventually, want to sell to Vietnamese consumers. The market behind the manufacturing story is where most Vietnam market research briefs originate — and where most international market assumptions fail first. For businesses evaluating business opportunities in Vietnam, the consumer question follows the supply chain question faster than most expect.

Vietnam at a Glance

Facts only [1][2][3]:

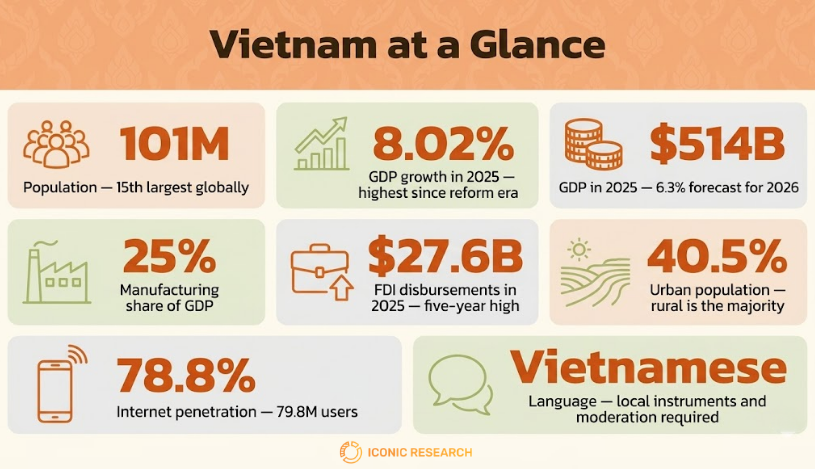

- Population: 101 million (2025). 15th largest globally.

- GDP: approximately $514 billion (2025) — 8.02% growth, highest since the reform era [1].

- GDP growth forecast: 6.3% in 2026 (World Bank) [2].

- Vietnam manufacturing: accounts for 25% of GDP. FDI disbursements of $27.6 billion in 2025 — five-year high, with 82.8% flowing into manufacturing and processing [1].

- Vietnam main industries: manufacturing and processing (electronics, textiles, footwear), agriculture, services, tourism, and a rapidly growing domestic consumer market.

- Business opportunities in Vietnam: driven by FDI inflows, a growing middle class, and accelerating digital commerce adoption.

- Urban-rural split: 40.5% urban — the lowest urbanisation rate in mainland Southeast Asia. Rural Vietnam is not peripheral; it is the majority [3].

- Digital penetration: 79.8 million internet users, 78.8% of the population [3]. 76.2 million social media users — 75.2% penetration.

- Language: Vietnamese. No English lingua franca. All research requires Vietnamese-language instruments and local moderation.

- Religion: majority non-religious with strong Buddhist, Confucian, and folk religious influences. Family and community remain the primary decision-making units in high-involvement purchases.

The Vietnamese Consumer

Vietnam’s consumer market is a market in formation. The Vietnam middle class that international businesses are entering to reach is not the middle class that will exist in five years. Research that captures a snapshot without accounting for the velocity of change produces market entry strategies that are obsolete before launch.

The Vietnam North-South Divide

The Vietnam north south dynamic is structural, not cosmetic. Ho Chi Minh City — the commercial engine — is more entrepreneurial, brand-open, and consumption-oriented. Hanoi — the political capital — is more conservative, relationship-driven, and sceptical of unfamiliar foreign brands. Brand trust built in HCMC does not automatically transfer north. Consumer research that treats Vietnam as one market produces findings that are accurate for neither city [4].

The Rural Majority

With only 40.5% urbanisation, the majority of Vietnam’s 101 million people live outside major cities [3]. Rural Vietnam has different income levels, different channel access, different brand relationships, and different purchase decision structures — typically family and community-mediated rather than individual. FMCG brands that validate in urban modern trade and project nationally routinely find their rural volume assumptions were built on the wrong consumer.

A Middle Class Being Built in Real Time

Vietnam’s middle class is expanding faster than the infrastructure and brand ecosystem built to serve it. Consumers who were not in the addressable market three years ago are entering it now — with different information sources, different aspirational reference points, and different brand loyalty patterns than established middle class consumers in Thailand or Malaysia. Research that segments the market without accounting for upward mobility misses the most commercially significant consumer cohort.

The Role of Family in Purchase Decisions

Despite rapid digitalisation and a median age of 33.4 years [3], high-involvement purchase decisions in Vietnam remain strongly family-mediated. A young urban professional may research a product independently and still defer the purchase decision to parents or a household consensus. Research designs that treat Vietnamese consumers as independent decision-makers underestimate the influence of family structure on conversion.

What the Manufacturing Brief Misses

The Supply Chain Assumption

Companies entering Vietnam as manufacturers often assume that understanding the production environment is sufficient. It is not — for those with any ambition to sell into the domestic market. The operational knowledge required to run a factory in Binh Duong is entirely different from the consumer knowledge required to sell to families in Da Nang or Can Tho. These are two separate research briefs, and the second is frequently not commissioned until after the first market entry investment is made.

The Urban Panel Assumption

Vietnam’s online research panels are concentrated in HCMC and Hanoi. A nationally representative study requires deliberate geographic stratification — HCMC, Hanoi, and a minimum of two to three provincial cities. Research conducted only through urban panels produces findings that represent approximately 40% of the consumer base. For FMCG, that means missing most of the volume.

The Vietnam Ecommerce Assumption

Vietnam ecommerce is growing rapidly — but social media engagement consistently outpaces purchase conversion, particularly in provincial markets where last-mile logistics remain inconsistent. Research that equates Facebook or TikTok engagement with purchase intent produces forecasts that overestimate online channel volume and underestimate the continued role of wet markets, traditional trade, and community-based distribution.

The Language Assumption

Vietnam has no English lingua franca. Research instruments designed in English and translated at execution — rather than designed in Vietnamese from the outset — introduce systematic instrument bias. Question structure, response scale framing, and concept language all require native Vietnamese design, not translation. This determines whether the research is measuring what it claims to measure.

Key Research Considerations for Vietnam

North-South Sampling

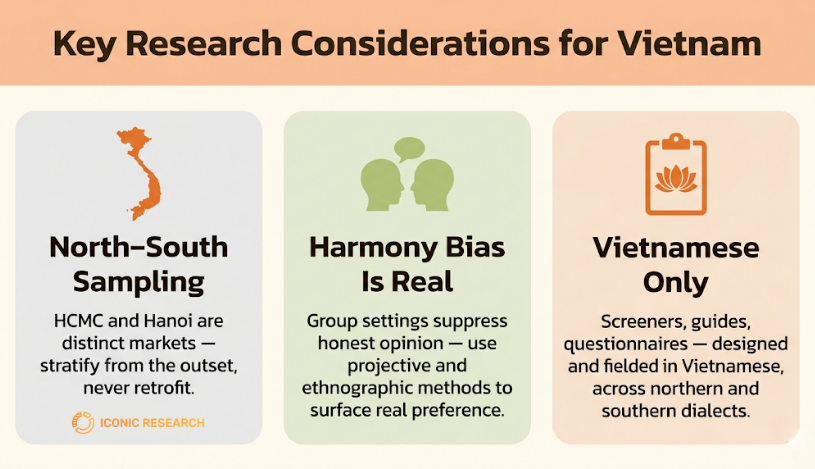

Every quantitative study in Vietnam requires deliberate north-south stratification — HCMC and Hanoi as a minimum, with provincial representation for nationally projectable findings. A focus group in HCMC and a focus group in Hanoi on the same topic will frequently produce different — and both valid — findings. Quantitative research design for Vietnam must build this into the sampling frame from the outset, not retrofit it after fieldwork.

Qualitative in a Hierarchical, Harmony-Oriented Culture

Vietnamese research settings exhibit strong social harmony bias — respondents avoid expressing opinions that might create conflict, particularly in group settings with moderators perceived as authority figures. Skilled qualitative research design uses projective techniques, paired interviews, and observed ethnographic methods to surface genuine preference rather than socially acceptable responses [5].

No English Instruments

All research instruments — screeners, discussion guides, questionnaires — must be designed and executed in Vietnamese. Iconic Research commissions local moderators and fieldwork partners with native Vietnamese fluency across both northern and southern dialects, ensuring that regional linguistic nuance does not suppress findings.

Multi-Country Coordination

Vietnam is frequently part of a broader ASEAN research programme — particularly for automotive, FMCG, and consumer technology clients running China plus one strategies alongside consumer market entry.

In practice, this means projects like a five-country simultaneous study for a global automotive brand evaluating consumer perception across ASEAN — including Vietnam — with local moderation coordinated across all five markets under a single brief. See case study.

For clients building comparable intelligence across ASEAN, Vietnam findings are most valuable when methodologically aligned with parallel studies in Indonesia and the Philippines. That comparability is a design decision made at briefing — not something that can be retrofitted after fieldwork.

Working with a Research Partner for Vietnam

International businesses entering Vietnam need a Vietnam market research agency that can navigate the north-south divide, design instruments in Vietnamese from the outset, and execute fieldwork across urban and provincial markets. The relevant questions: Does the agency have in-country fieldwork partnerships in both HCMC and Hanoi? Can they recruit and moderate in Vietnamese with regional dialect sensitivity? Do they understand the category dynamics of your sector?

Iconic Research is a Bangkok-based market research company coordinating international market research programmes through established long-term fieldwork partnerships across Ho Chi Minh City, Hanoi, and key provincial markets. Research is designed from Bangkok, executed in-country, and delivered as unified findings — whether Vietnam is the sole market or part of a broader ASEAN programme. See fieldwork and recruitment for how we structure in-country execution.

For clients who have entered Thailand first and are expanding the ASEAN footprint, the research model is consistent. See market entry Thailand for the reference model.

Frequently Asked Questions

What does market research in Vietnam involve?

Consumer landscape research across north and south, urban and rural. Product or concept testing with Vietnamese consumers, in Vietnamese, across representative geographies. Distribution research across modern trade, wet markets, and social commerce channels.

How is the Vietnam north-south divide relevant to research?

HCMC and Hanoi are different consumer markets — different brand openness, different decision-making styles, different trust pathways. Every study requires dual-city design at minimum.

What does doing business in Vietnam require from a research perspective?

Understanding which Vietnam you are entering — HCMC-centred commercial market, Hanoi-centred institutional market, or provincial consumer channels. Each has a different research brief and a different competitive landscape.

Does Iconic Research conduct fieldwork in Vietnam?

Yes — through long-term partnerships across HCMC, Hanoi, and provincial markets, in Vietnamese, with Bangkok quality control. Vietnam has run as part of multi-country ASEAN programmes including a five-country automotive study.

What sectors does Iconic Research cover in Vietnam?

Manufacturing-adjacent consumer research, FMCG, automotive, healthcare, financial services, technology, and market entry for international brands moving from supply chain to consumer market presence.

References

[1] General Statistics Office of Vietnam (2026). Socio-Economic Situation Q4 and Full Year 2025. https://www.nso.gov.vn/en/data-and-statistics/2026/01/socio-economic-situation-in-the-fourth-quarter-and-2025/

[2] World Bank (March 2025). Taking Stock: Viet Nam Economic Update. https://www.worldbank.org/en/country/vietnam/publication/taking-stock-viet-nam-economic-update-march-2025

[3] We Are Social / Meltwater (2025). Digital 2025: Vietnam. https://datareportal.com/reports/digital-2025-vietnam

[4] The Investor VN (2026). Vietnam’s 2025 FDI Disbursement Hits 5-Year High. https://theinvestor.vn/vietnams-2025-fdi-disbursement-hits-5-year-high-d18057.html

[5] Iconic Research. Qualitative Market Research. https://iconicthai.com/services/qualitative-market-research/

If you wish to quote any information from this article, please kindly cite the source along with the link to the original article to respect copyright. |

Iconic Research Thailand Your trusted partner in market research and consulting across Thailand and Southeast Asia. Headquartered in Bangkok, we provide research-driven insights across the Philippines, Malaysia, Indonesia, Singapore, Laos, and Vietnam. We help businesses navigate Thailand's market complexities through consumer insights, market entry strategy, and trend foresight. Contact us if you have any queries! (+66)888 954 954 |

Contact us

We always looking for new and exciting opportunities. Let’s connect.

Related posts

Key Opinion Leader: What Thai Brands Should Research Before, During, and After a KOL Campaign

Key Opinion Leader: What Thai Brands Should Research Before, During, and After a KOL Campaign

Platform metrics mislead brands choosing and measuring KOLs in Thailand. A research-first look at what to verify before, during, and after a campaign.

10 min read Customer Persona: Build One That Reflects Real Thai Consumers

Customer Persona: Build One That Reflects Real Thai Consumers

Most Thai brands have customer personas built from assumptions. Research-backed personas reveal a different consumer — and drive different decisions.

9 min read Consumer Insights: What the Data Doesn’t Tell You About Thai Consumers

Consumer Insights: What the Data Doesn’t Tell You About Thai Consumers

Consumer insights explain why Thai consumers behave as they do. The challenge is not collecting data — it is collecting data that actually reflects reality in a market where standard research instruments systematically mislead.

9 min read